(source: allbankingsolutions.com)

What is TDS?

The full form of TDS is Tax Deducted at Source. Thus, when someone deducts tax at appropriate rate at the time of making payment, then the amount deducted is known as tax deducted at sources. One of the most often case for such TDS is the deduction of the tax on the interest paid on Fixed deposits to you by all banks. From FY 2015-16 onwards, TDS is also applicable for Recurring Deposits. However, there is no TDS for interest earned on Saving Bank accounts.

- (A) Tax Exemption : For FY 2015-16 (also for FY 2014-15 :Interest earned in Saving Bank accounts upto Rs 10,000 is exempted from Tax (moreover, no TDS is applicable even if the interest earned is more than Rs10,000/-. Interest income above Rs10,000/- is fully taxable. However, interest income from other kind of deposits (like from Fixed Deposits (also called term deposits) / Recurring Deposits ) are NOT exempted from tax. Thus, feel free to keep upto Rs 2 lakhs in Saving Bank accounts as most of the banks pay 4% interest in saving bank accounts. Even if you keep high amount in Saving Bank account, there will be no deduction of TDS. You will need to pay tax for the interest earning in Saving Bank accounts if the total interest in saving bank account exceeds Rs 10,000/-

- (B) Deduction of TDS : As explained above, No TDS is deducted by banks on interest earned in Saving Bank accounts. However, interest earned on Fixed Deposits and Recurring Deposits are subject to deduction of tax as per rules (Earlier Recurring Deposits were exempted from TDS but now from June 2015 onwards, banks are required to deduct TDS even on the interest earned on Recurring Deposits). As far as interest earned on Saving Bank accounts is concerned, income from interest earned on Saving Deposits beyond Mr 10,000/- p.a.only are taxable. Thus, in nut shell we can say that NO interest income from Fixed Deposits or Recurring Deposits is exempted from income tax. As explained above, now TDS is deductible on interest earned on Fixed Deposits / Term deposits and also on Recurring Deposits. However, in certain conditions, no TDS is deducted even on the interest earned on fixed deposits, e.g. if the total interest earned on such deposit in a financial year is upto Rs.10,000/-. However, you should be clear in your mind that even if No TDS is deducted on your interest earned on Fixed Deposit interest or Recurring Deposit, you still have to include this income in your tax return and pay tax.

- (C) Rules for Deduction of TDS on interest paid / accrued : As per present income tax guidelines, banks are required to deduct tax at source (TDS) on deposits if the total interest earned on all your fixed deposits / recurring deposits in a bank (at all branches of the bank) is more than Rs.10,000 in a financial year. (as per these guidelines even if a fixed deposit is in the name of a minor TDS is deducted). However, the depositors can claim the credit for such TDS in their income tax returns. (Now a days such deducted TDS is reflected in AS26 which can be downloaded and checked before you submit your income tax return. (Even in case of minors, this credit for TDS can be claimed by the person who manages the minor's income).

- Remember, now a days as and when a bank pays an interest on the fixed deposits / recurring deposit, it checks whether the account is exempted from TDS. If it is not exempted, then TDS is deducted. You should also remember that TDS is deducted even on interest accrued in case of Fixed Deposits / Recurring Deposits (but not yet paid) at the end of the financial year i.e. 31st March every year.

We can summarise the above details in the following table :

Interest Earned on

|

Whether TDS is Applicable

|

Whether Income Tax is Payable on Interest income

|

How to Avoid TDS

|

Saving Bank Accounts

|

No

|

Income Tax is payable if the interest income earned on all saving bank accounts is over Rs10.000/-. No tax is payable for interest income in SB accounts upto Rs 10,000/-.

|

No Need to worry as no TDS is deducted

|

Fixed Deposits

|

Yes, if the interest income from all such deposits exceeds Rs10,000/- in a FY. (TDS is deducted at 10% if PAN submitted or else it will be deducted at 20%)

|

Interest earned is fully taxable and full interest income (including accrued) should be included as your income at the time of filing the IT return. However you can claim credit for all the TDS deducted by your bank for which bank has given you Form 16-A and shown in AS26.

|

Submit Form 15 G / 15 H, if you are eligible to submit the same. (See the details given below)

|

Recurring Deposits

|

Yes, if the interest income from all such deposits exceeds Rs10,000/- in a FY. (TDS is deducted at 10% if PAN submitted or else it will be deducted at 20%)

|

Interest earned is fully taxable and full interest income (including accrued) should be included as your income at the time of filing the IT return. However you can claim credit for all the TDS deducted by your bank for which bank has given you Form 16-A and shown in AS26.

|

Submit Form 15 G / 15 H, if you are eligible to submit the same. (See the details given below)

|

Some Queries answered in Question-Answer format :

(a) Whether Interest Income on Fixed Deposits and Recurring Deposits from Bank is Taxable ?

Yes, the interest income on fixed deposits and recurring deposits is now fully taxable, as shown in the table above. On such incomes banks are required to deduct TDS (From FY 2015-16, even the interest accrued on Recurring Deposits will be liable for TDS). Such an income comes under the head “income from other sources”. Banks are required to deduct TDS in the following cases and the rates mentioned below : -

If interest earnings from your fixed deposits exceed Rs. 10,000 in a financial year, then Bank deducts TDS (Tax deduction at source) as per the following criteria.

(a) If you have provided PAN details to the Bank then Bank would deduct TDS at the rate of 10 %.

(b) In case you have not provided the PAN details then Bank would deduct TDS at the rate of 20%.

(C ) Whether We Can avoid TDS to be deducted by Bank :

Yes you can submit avoid deduction of TDS provided you are eligible for the same. As per the present guidelines, who does not want TDS to be deducted needs to declare that his / her income is below the threshold limit for filing an income tax return. The following forms are used for this purpose :-

· Form 15G- It is applicable for Individual below 60 years, HUFs and Trusts.

· Form 15H- It is applicable for individuals above 60 years.

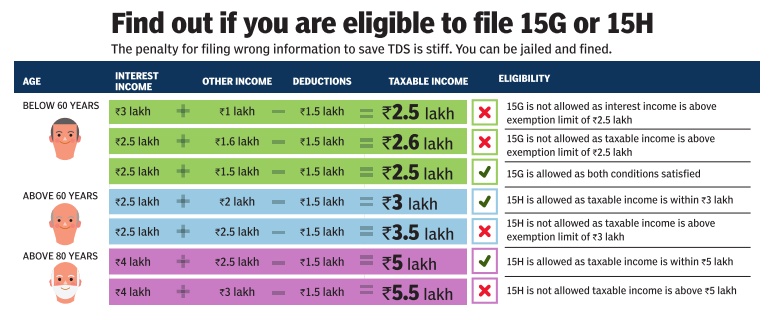

(D) What is the Eligibility criteria for submitting declaration forms 15G or 15H to Banks:

Following two conditions needs to be fulfilled by you for the submission eligibility of Form 15G or 15H.

1. The final estimated total income calculated as per the income tax rules and provisions should be NIL.

2. Total interests earning should not cross the basic exemption limit of Rs.2,50,000.

The above will be more clear through the following example:-

Shri Sunil Kumar, Age 55 years earns Rs. 2,60,000 from Interest from bank fixed deposits and he also earns Rs. 40,000 from other sources. Thus, his total income is Rs.3,00,000/- for the Financial Year.

During the FY he invests Rs. 1,50,000 in Public Provident Fund (PPF). Now, we can find out whether he is eligible to submit Form 15-G to avoid TDS :-

(a) Check whether he is eligible as per 1st Rule : In terms of income tax regulations, his total estimated income is not taxable (Total Income Rs 3,00,000-Investment Rs 1,50,000 = 1,50,000). Thus he fulfills the criteria under Rule 1 specified above.

(b) However, total estimated interest earnings are Rs2.60 lakhs. This is higher than the interest exemption limit of Rs. 2,50,000 as per the 2nd criteria. Thus he has not fulfilled the 2nd criteria.

Hence, he is not eligible to submit the form 15G. In this condition, Banks would deduct the TDS on earning interest and later he can claim the excess tax deducted at the time of filing of his return of income.

We give below a diagram, which will make it much more clear as to whether you are eligible to file 15G / 15 H form:-

- Remember that : -

- (a) Even if you submit the 15G / 15H Form, the tax which has already been deducted by way of TDS during the year prior to submission of 15H Form, is usually not refunded by the bank as they are under obligation to deposit this TDS within a time bound period. . However this TDS certificates will be issued to the customers which he / she can use while filing his/her tax return and get credit for the same.

- (c) 15G/15H Forms are valid only for the particular financial year in which they are submitted to the bank.

- (d) In view of above, usually banks ask that a fresh 15G / 15H form for each deposit that is placed with the Bank

- (e) However, if the depositor furnishes form 15G / 15H (which are available free of cost from all banks) and therein declares he / she does not have tax liability at all, the bank will not deduct any TDS from the interest earned by the depositor.

- (f) Thus, the above, in a nutshell indicates that if the interest income from a bank branch is more than Rs.10,000/- (and you have not submitted form 15G / 15H), the Bank will deduct the TDS. For any TDS deducted by the bank, it will issue a Form 16A which can be used while filing the income tax returns. Such TDS is also reflected in the AS26 form which can be generated from income tax website.

- (g) Thus, in case you do not want the TDS to be deducted, you can split your Bank Deposits in two or more Banks so that the total interest earned at one Bank is less than Rs.10,000/-. (However, remember this does not mean that income earned from such deposits is exempted from income tax. You have to club all such interest income and add to your other income, and pay the tax while filing the income tax return.)

In Income Tax law, one of sources of the income is "Interest Income" and thus directions issued by income tax authorities have to be followed by all bankers.

What are the rules for deducting tax on fixed Deposit ? When do the bank deduct TDS on a fixed deposit? :

Banks deduct tax (TDS), if the total interest earned on all your fixed deposits in the bank is greater than Rs.10,000/- during a financial year. The tax liability for the purpose of TDS was earlier determined at the branch level. The bank branches used to check interest on your fixed deposits at a particular branch only as it was impossible to club the interest earned in other branches. However, after introduction of CBS, now banks are able to club such interests at different branches if Customer ID / PAN is same. Thus, if interest earned on fixed deposits in different branches exceeds the threshold, the TDS will be deducted by the system. TDS is also deducted on interest accrued (but not yet paid) at the end of the financial year viz. 31st March every year.

- Difference between form 15G and 15H (Free Download form 15G) (Free Download form 15H) : The form 15G and 15H are submitted to banks by depositors who DO NOT want that TDS be deducted from their interest earned on fixed deposits. A person who is below 60 years can file the Form 15 G . However, only a person of 60 years or more is eligible to file Form 15 H. There are some other major issues relating to 15G and 15 H and the same are discussed below:-

Difference between Form 60 and Form 61 (Free Download form 60) (Free Download form 61)

- FORM NO. 60 :[See second proviso to rule 114B] : Form of declaration to be filed by a person who does not have a permanent account number and who enters into any transaction specified in rule 114B. Form of Declaration to be filed by a person who does not have either a Permanent Account Number or General Index Register Number and who makes payment in cash in respect of transactions specified in clauses (a) to (h) of rule 114BFORM NO. 61: [See proviso to clause (a) of rule 114C(1)]. Form of declaration to be filed by a person who has agricultural income and is not in receipt of any other income chargeable to income-tax in respect of transactions specified rule 114B. Form of Declaration to be filed by a person who has agricultural income and is not in receipt of any other income chargeable to income tax in respect of transactions specified in clauses (a) to (h) of rule 114B(Updated in August 2015)

Hindustan Copper Limited Recruitment Notification 2017

ReplyDeleteDownload TSPSC Beat Officer,Section Officer posts Hall Tickets 2017